Plumbing & Heating May sales up 12.2% year on year

![]()

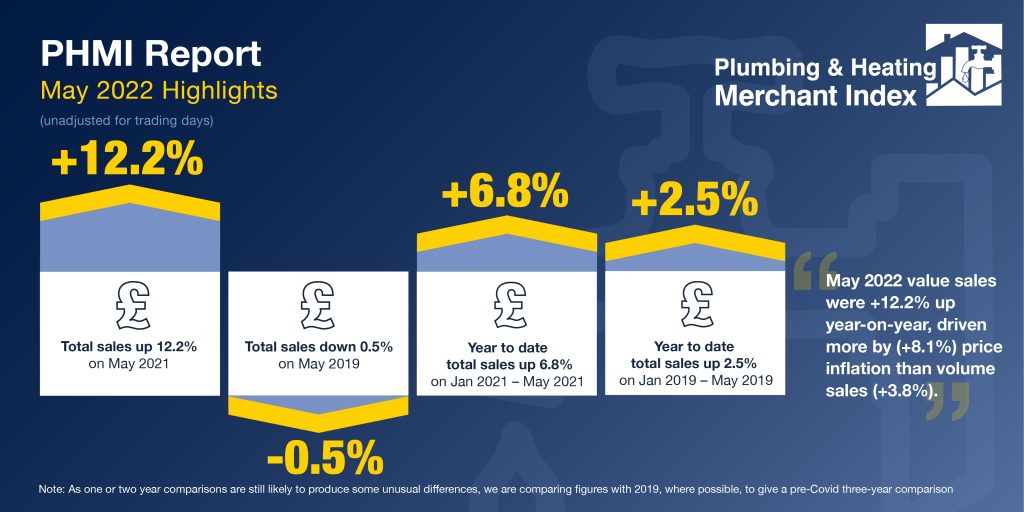

The latest figures from the Plumbing & Heating Merchant Index (PHMI) report show total value sales for May 2022 through specialist plumbing and heating merchants climbed +12.2% compared to May 2021.

This growth was driven in part by price inflation (+8.1%) but volumes were also up (+3.8%). With an extra trading day in May 2022, like-for-like sales were +6.6% higher.

Compared to May 2019, a more normal pre-Covid year, total value sales for May 2022 were flat (-0.5%), with one less trading day this year. Like-for-like sales were +4.5% up.

Month-on-month sales data showed that May sales were +7.1% higher than April 2022, with one extra trading day in the most recent period. Like-for-like sales were +1.8% up. Against trend, volume rose +8.0%, while prices fell -0.8%.

Year to date value sales in the period January-May 2022 were +6.8% higher than the same period in 2021, with no difference in trading days. Price inflation reached +7.5% while volume was down -0.7%.

Plumbing & Heating merchants’ sales in the last 12 months (June 2021 to May 2022) were +0.9% up on the previous 12-months with one less trading day in the most recent period.

Mike Rigby, CEO of MRA Research, which produces the report comments: “Soaring price inflation gives the illusion of strong growth, and May did grow in terms of volume, but year to date volumes are marginally down.

“The cost-of-living crisis is knocking consumer confidence, which is plumbing new depths. While this is not having have much impact on older homeowners with little or no mortgage, younger homeowners (under 45s) are feeling the pressure of doubling energy bills and higher food costs, particularly if they have families to support. For them, home improvement projects are now lower down the priorities list, outside of essential repairs and maintenance, so a tail off in RMI-related sales is inevitable. How long will that last? Industry forecasts by Glenigan predicts a strong three year recovery starting next year.”

In a comment on the methodology and scope of data, Mike said: “This month we can see the effects of recent changes to the composition of the PHMI. Currently, the plumbing and heating merchant sector is settling down after a bout of intense M&A activity. We expect more merchants to contribute data, and coverage to grow once these structural changes have worked themselves through.

“As a result of changes in ownership, and new group formation, some merchants have left and some joined the PHMI. The net effect in those contributing sales data to GfK’s merchant panel is a reduction in national branch coverage from 81% to 73% of the market, still the bulk of the market.

“An unexpected effect of the changes, is that companies contributing sales data in the PHMI appear to be growing faster than the market as a whole. M&A activity and new group formation is inherently disruptive, so perhaps that is not surprising in the short to medium term. GfK will be reviewing trends, but after the upheaval from Covid and the bounce back, and now this structural change, we expect the trends to stabilise.”

The Plumbing & Heating Merchant Index (PHMI) is the first to analyse point of sales data collated from specialist plumbing & heating merchants with combined annual sales of £3bn, to chart their performance month-to-month.

Based on data from GfK’s Plumbing & Heating Merchant Panel, which represents over 70% of the market by value, the report provides reliable data and a platform and voice for the industry, as well as for leading plumbing & heating brands. It is produced by MRA Research for the Builders Merchants Federation. There is no overlap or double counting between PHMI and the Builders Merchants Building Index (BMBI) sales data.

To download the latest report, or learn more about becoming an Expert, speaking on behalf of your market, visit www.phmi.co.uk.